6 Money-Saving Questions You Should Always Ask Your Doctor

Don’t be shy. A few simple inquiries can reduce your out-of-pocket costs on medical care and medications, saving you hundreds of dollars — and sometimes even thousands.

Everyone is budget-conscious these days, yet healthcare costs are rising rapidly. According to the Centers for Medicare & Medicaid Services, healthcare spending in the United States grew by 9.7% in 2020, and healthcare costs averaged $12,530 per person. And in 2019, the U.S. spent $1,126 per person on prescription medications alone, according to the Peterson-KFF Health System Tracker.

That’s a significant hit to anyone’s wallet — so what can you do to save? Start by having an open conversation with your doctor. A simple discussion during your appointment could help you save money on treatments and care, as well as on medications and prescriptions.

“Your provider doesn’t automatically receive notice about how much a medication costs or what the copay is at your pharmacy,” explains Alyssa Wozniak, Pharm.D., a board-certified pharmacotherapy specialist and Clinical Assistant Professor at D’Youville School of Pharmacy in Buffalo, New York. “They might not be aware that your medication is too expensive unless you tell them. They can work with you to determine a more affordable option so that you can continue taking your medications without causing financial burden.”

Here are six important questions to ask your doctor that may help you save money on your medical expenses.

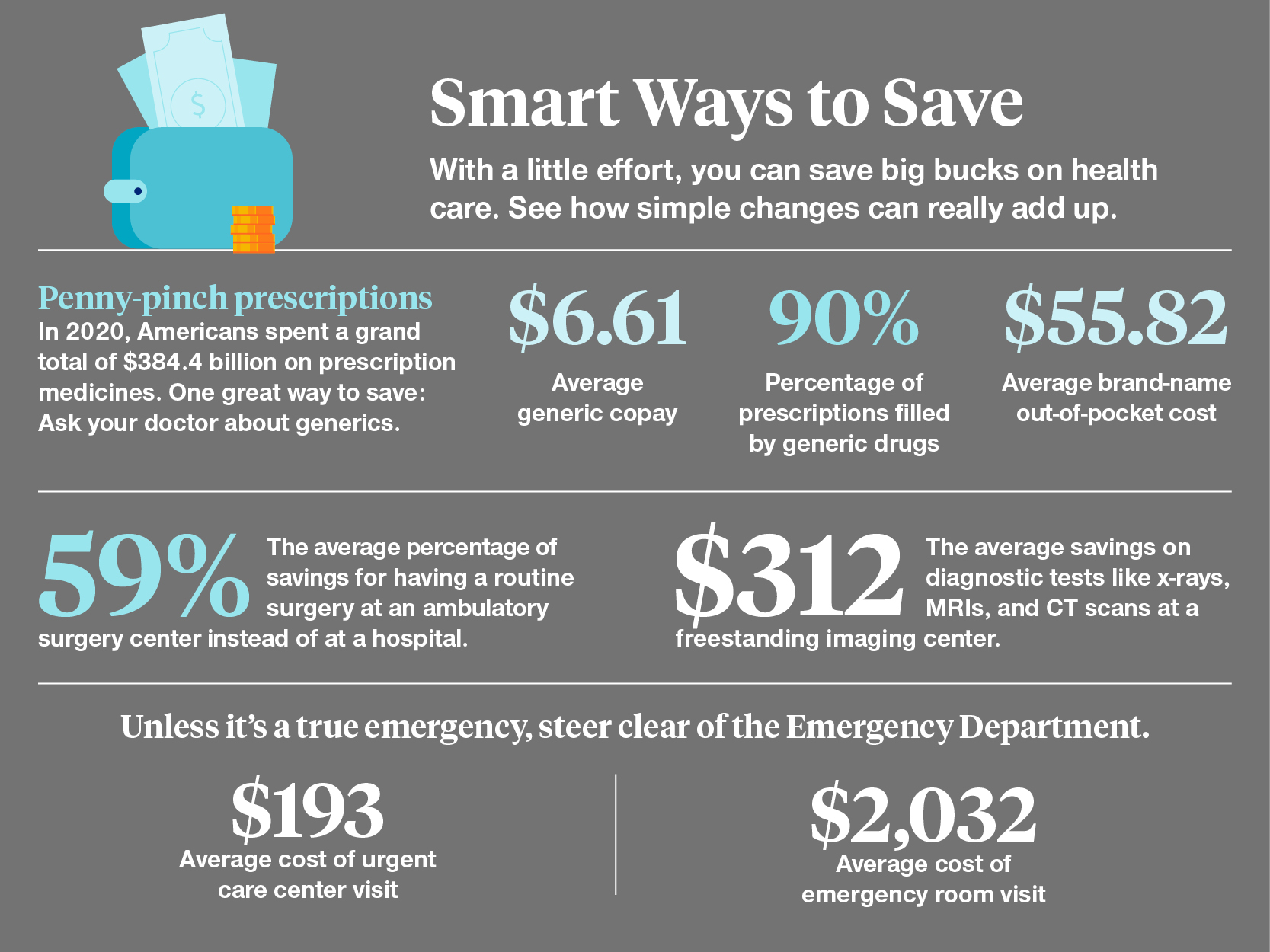

Question #1: Is there a nonhospital imaging center nearby?

“Big hospital systems charge more and bill higher for the same services you can get at a smaller imaging center,” says Noor Ali, MD, a health insurance adviser. “You can receive the same service and same quality, but your out-of-pocket cost will be less simply because of the facility you choose.” (Learn how to save on your next MRI.)

Question #2: Is there a less expensive version of this medication?

“Some of the options in a medication class may have lower copays if they are generic,” says Wozniak. “If you ask, your provider can review the formulary for your specific insurance plan and prescribe cost-savings options if appropriate for your care.” (The formulary is the list of prescription drugs covered by your insurance plan.)

Question #3: Can I have this procedure done at an outpatient facility?

“Inpatient facilities come with tons of fees, for everything from the room and food to nursing services and equipment use,” says Dr. Ali. “For simple in-and-out, same-day surgeries, opting to have them done at an ambulatory outpatient center will help you avoid all those service charges.” (To compare costs on medical services or procedures, go to Turquoise Health.)

Question #4: Does my insurance cover this medication?

“It’s important to always let your doctor’s office know what insurance you have. In the case of medications, sometimes patients have a different prescription insurance card or carrier than their regular medical coverage,” says Wozniak. “Have that prescription coverage information on hand so that the provider can choose medications that are best suited to your plan’s formulary and copay structure.”

She adds that it’s also important to inform your doctor if you don’t have prescription insurance so that they can be extra mindful of medication costs when writing you a prescription.

“Your provider can refer you to other members of the healthcare team to help you get signed up for prescription insurance, if warranted,” says Wozniak.

Question #5: If a medication is not covered by my insurance, do I have any other options?

“Often your insurance covers some drugs in a class of medications, but not the entire class,” says Wozniak. “Your provider might be able to work with you and choose an option that’s included on your insurance formulary.”

She adds that in certain cases, however, the medication and any comparable alternatives might not be covered by your insurance at all. In those situations, your provider might be able to pursue prior authorization to get it covered. Or they may explore options such as patient-assistance programs that provide the medication directly from the manufacturer, depending on the patient’s specific circumstances.

“Many medications do have coupons that serve to minimize costs. It’s important to review the terms of the coupon with your provider, however,” says Wozniak.

For example, she explains that a copay-reduction coupon cannot be combined with Medicare or Medicaid insurance plans, but free trial offers for certain medications can be. And other times, the coupon may have a spending limit.

There are also coupon services like Optum Perks. You search for your medication, compare prices at local pharmacies, then print, email, or text your coupon and show it to the pharmacist. (Get more tips on how to save on medications.)

Question #6: Can I get my issue resolved with a virtual medical consultation rather than an in-person visit?

“Virtual medical care has grown in popularity, especially during the pandemic,” says Dr. Ali. “In addition to saving tons of time, virtual visits can have zero or low copays for the same medical advice you’d receive in the office.”

Additional sources

National Health Expenditure Data: Centers for Medicare & Medicaid Services

How Prescription Drug Costs in the U.S. Compare to Other Countries: Peterson-KFF Health System Tracker

The Benefits of a Health Insurance Adviser: Dr. Noor Ali